Pet insurance functions in a similar manner as human health insurance – pet owners pay a monthly premium, and depending on the type of plan and specific terms, the insurance policy covers a portion of certain treatments and procedures. While many plans cover unexpected medical issues, some plans offer some level of coverage for basic preventative care as well. Like human health insurance, the specific procedures and treatments covered – and to what extent they’re covered – varies by plan, and most plans don’t cover pre-existing conditions (conditions your pet has been diagnosed with prior to obtaining pet insurance coverage).

Find the Cheapest Pet Insurance Quotes in Your Area

Deciding whether to purchase pet insurance is a decision that should be made while a pet is young, but young pets are typically healthier. While it can seem as though you’re paying a premium for something you’ll rarely or never use, many pets develop chronic or life-threatening conditions at some point throughout their lives, and treating these conditions can be quite costly. Is pet insurance worth the cost, and is it something every pet owner should purchase for their pets? Read on to learn about some of the factors to consider.

What Is the Average Cost of Pet Insurance?

When deciding whether pet insurance is a good buy, it’s helpful to take a look at the hard numbers. The cost of pet insurance is going to vary drastically, depending on how old your pet is, what type of plan you choose, and which company you decide to purchase the insurance from. Younger pets might have a premium of $15 or $20 per month, while you might be paying many times that for older pets. The average annual cost of pet insurance for pets of all ages is a little over $500 per year, or about $42 per month.

Now let’s think about what you are likely to pay for veterinary care over the course of a year or your pet’s lifetime. In 2017, the average annual vet bill was $92. This seems to take into consideration people who do not take their pet to the vet annually as well as those whose pets needed care in addition to a routine exam and vaccinations. Keep in mind that most pet insurance plans will not pay for routine care unless you purchase a rider to cover preventative services.

At first glance, you might think that pet insurance isn’t a worthwhile investment, but then consider how much treatment costs for common illnesses and conditions. Diabetes in dogs, for example, requires medications and supplies that can cost up to $150 per month. Chemotherapy for a pet with cancer can cost thousands of dollars, as can surgery for various conditions. ACL surgery in dogs can cost up to $20,000. On the other hand, most dogs and cats don’t end up with cancer or ligament injuries; in that case, a more common condition like vomiting or an ear infection will cost hundreds, not thousands. And, of course, many pets don’t need any care for injuries or illnesses in some (or even most) years.

If your pet needs specialized care at any point, then pet insurance is a good way to ensure that you will be able to get him the care he needs. Conversely, if your pet is gifted with good health and good luck, you might never recoup the costs of the premiums.

Do I Really Need Pet Insurance?

As outlined above, the question of whether you need pet insurance can only be answered with “it depends.” If your pet is never sick or injured, then you don’t need pet insurance. If he is, however, then it’s typically a good investment. The problem is that you won’t know whether or not your pet will have an issue until it happens. Remember that most pet insurance policies have a waiting period for care resulting from an illness or injury, so you cannot simply decide to get coverage on the day that your pet becomes ill or injured.

Here are some of the pros and cons of pet insurance to keep in mind.

Benefits of Getting Pet Insurance

- You will be able to get your pet the care he needs if he is injured or ill. Many pet owners find that they have to put off care for their fur babies because the expense is too high. Pet insurance can minimize or eliminate this concern.

- You might be able to get wellness visits covered. Some pet insurance companies have coverage for preventative or routine care. This means that vaccinations, spay/neuter surgery, and even monthly parasite medications can be reimbursed, in some cases.

- You can see whichever veterinarian you want. Unlike health insurance for humans, pet insurance coverage does not depend on seeing an in-network vet. You will be submitting the claims yourself, so it won’t matter who you see for the care.

- You might be eligible for a discount. Working for certain employers or belonging to an organization such as AAA might entitle you to a discount with certain pet insurance companies. Once you decide to get pet insurance, look into this by asking your HR representative and inquiring with any organizations that you belong to.

Drawbacks of Getting Pet Insurance

- You might pay more in premiums than you would spend for care. Since you do not have a crystal ball to tell the future, you don’t know ahead of time if this will be the case. If your pet does not need anything other than routine care, then you will end up paying more than you save.

- There might be waiting periods. Most pet insurance policies will include a waiting period, so it is important to know when you will be able to access care and have your claims paid.

- Reimbursement levels can vary. Depending on the plan that you choose, you might have services reimbursed at anywhere from 60 to 90 percent. Be aware that pet insurance will not cover all expenses related to a claim; you will almost always have to pay out a percentage on your own. In addition, you might have a deductible and/or an annual maximum to keep in mind. Be sure to read the fine print and ask questions if you do not fully understand the plan.

Who Has the Best Pet Insurance?

While everyone should do their due diligence and choose a plan that works best for their individual needs, we have a top pick in mind when it comes to the best pet insurance company.

Learn More on Embrace Pet Insurance’s secured website |

Average Customer Rating What we like: |

|---|---|

| Monthly Premium | As low as $10 for cats and $16 for dogs |

| Deductible | $200, $300, $500, $750, or $1,000 |

| Benefits Limits | 70%, 80% or 90% of annual costs |

| Age Restrictions | As young as 6 weeks and as old as 14 years |

|

Visit the Embrace Pet Insurance website or get a quote for pet insurance |

|

Our top pick is Embrace Pet Insurance for a variety of reasons. You learn more and read our full review here.

You can also see our full list of The 5 Best Pet Insurance Companies.

What Do the Experts Say?

To find out what the experts think, we reached out to a panel of veterinarians, pet bloggers, and pet insurance professionals and asked them to answer the question of whether pet insurance is worth it. These are individuals who work with pets and their human families day in and day out, so they have some great insight to share.

Meet Our Panel of Veterinarians, Pet Bloggers, and Pet Insurance Experts:

Read on to learn what our experts had to say about whether pet owners should purchase pet insurance and whether it’s a worthwhile investment.

Holly Ganz

Holly Ganz

Holly, co-founder and CEO of AnimalBiome, is a microbial ecologist with a BS from George Washington University, a MS from Scripps Institution of Oceanography, and a PhD from UC Davis. She was a postdoctoral fellow at UC Berkeley. Prior to creating AnimalBiome, she studied microbes in dogs and cats at the UC Davis School of Veterinary Medicine and the UC Davis Genome Center.

“In my personal and professional opinion, pet insurance is worth it…”

On the recommendation of our veterinarian, we enrolled Yuki, our 15-year-old Border Collie shepherd mix, in Trupanion pet insurance at the age of 11. She already had several pre-existing conditions that required regular care, including an autoimmune-related skin condition, arthritis, and urinary incontinence. We weren’t sure whether it would be worth it to enroll Yuki in pet insurance because she already had so many conditions that wouldn’t be covered, but we took a chance and went for it – and we are so glad we did. Just a few years after she enrolled, Yuki developed pancreatic cancer which had already spread to part of her liver. Trupanion covered 90% of the cost of the $6,000 surgery to remove the cancer; their financial contribution was invaluable to us. Having pet insurance for Yuki gives us the peace of mind that we’ll be able to pay for whatever treatment she needs to stay comfortable and content.

Meg Marrs

Meg Marrs

Meg Marrs

Meg MarrsMeg Marrs is the senior editor at K9 of Mine, a dog care website dedicated to helping owners better care for their four-legged buddies.

“The value of pet insurance really depends on what kind of investment you’re willing to put in if your dog or cat becomes ill…”

Would you be willing to cash out your life savings for another year with Fido if he gets seriously sick? Or would you be OK with letting your pooch go. This isn’t to pass a personal judgment on anyone – some folks wouldn’t be interested in spending money to prolong their dog’s life. If you know you’d sell your car and mortgage your home to heal your dog, then pet insurance is probably worth considering, as it won’t force you to such extreme measures in the event something does go wrong.

Another aspect to consider is your dog’s breed. The truth is that purebred dogs tend to suffer from more health issues than mixed breed dogs. That goes double for snub-nosed dogs who suffer from respiratory issues and giant breeds who are riddled with joint issues. If you have a dog who you already know is susceptible to health problems, pet insurance will most likely be a smart investment.

As always, do your research! Figure what your policy covers (just as you would with human health insurance) and calculate what your monthly cost will be to ensure that you have a plan that will work for your financial situation long term.

Rex Talbott

Rex Talbott

Rex TalbottRex Talbott is the Vice President of Business Development for Embrace Pet Insurance.

“If their pet’s well-being is a top priority, then owners should absolutely have pet insurance…”

It provides them with significant peace of mind from having to finance the costs associated with unexpected accidents or illnesses in their pet’s lives.

Being able to make a life-saving decision for your pet is invaluable, and for that reason pet insurance is worth it. We understand that those who do not use their pet insurance policy may feel that the cost is not worth the coverage. This is why Embrace Pet insurance offers personalized polices to fit any budget.

Walt Capell

Walt Capell

Walt CapellWalt Capell is the founder & CEO of The Insurance Shop, LLC.

“We treat our pets as family…”

And when they become sick or get into an accident we want to do everything we can to bring them back to perfect health. Unfortunately, many pet owners are faced with a tough decision when presented with costly invoices for treatment. According to the American Society for the Prevention of Cruelty to Animals (ASPCA) a medium-sized dog will cost its owner nearly $1,600 the first year, $1,000 for a cat, and roughly $500 a year after that (cat and dog), increasing as the age of the pet does. Pet insurance can greatly offset annual spending; as a highly customizable form of insurance, it can be written to fit any aged pet or owner’s budget. It covers everything from prescription food and medications to chemotherapy and acupuncture, without limiting owners to any network or veterinarian. Pet insurance can also help pay for many preventative care services such as spay/neuter surgeries and dental exams.

When a pet owner insures their pet, he/she is preparing for the unexpected, saving money on healthcare, and helping to assure their furry loved one will be a member of the family for many years. Whether or not the cost is a value to each individual person depends upon their individual financial situation and their unique relationship with their pet.

JC Matthews

JC Matthews

JC MatthewsJC Matthews is a licensed life and health insurance agent with over 9 years of experience in the industry and Co-Founder of Simply Insurance.

“I tend to look at this question the same way as if a pet parent asked me if I think they need health insurance…”

The answer will be 100% yes.

From my experience, pet parents are named that because they think of their pets as their kids and often refer to them as their furbabies. I think any parent would agree that health insurance for their child is very important.

The cost of a pet insurance plan will vary based on the type of pet that you have. However, in general, the rate will be reasonable for the type of pet you have and their usually common health conditions. When asking if it’s worth the cost I say 100% yes.

Medical bill put more and more people in debt every year and you shouldn’t let the same thing happen with your pet. A car accident or unexpected surgery could put you back thousands. While it’s easy to pay $30.00/month for a basic pet plan, coming up with $2,000 for an unexpected expense can put some people in financial ruin or cause their pet to have a very low quality of life or to pass away.

If your pet is a part of your family, then just like any family member, they need health insurance.

Deborah J. Turner

Deborah J. Turner

Deborah J. TurnerDeborah J. Turner, CPCU, AAI President of Dean Insurance Agency, Inc. in Altamonte Springs, Florida. The combination of her love of dogs, research about them and her intimate knowledge of the insurance industry, resulted in her developing a Canine Liability Policy to protect owners should their dogs ever injure another person or animal.

“If your dog bites, scratches, scares, trips a person, runs in front of a car causing both property and bodily injury…”

Are you sure your homeowner’s or tenant’s policy will cover you? Have you checked to see if there is a sub limit in your policy for animal liability?

Often the injuries may be a result of provocation, yet in many states you have no defense to protect you or your dog. Courts often require the dog owner to pay all expenses of the injured party. The cost of veterinary care has exploded – there are claims topping $20,000 to save a dog that has been badly injured by another dog. Injuries to children are far more expensive, often reaching hundreds of thousands of dollars, and claims may remain open until the child is 18 years old in the event additional plastic surgery is needed. Or, you could find yourself replacing a totaled vehicle if your dog slips his/her collar and runs in front of a car.

Today people are suing dog owners even if they are never touched by the dog. If someone just sees your dog and runs for their life, they likely will sue you if they are injured in their escape.

Should you carry canine liability insurance?

If your primary residence policy does not cover you adequately, then to assume your sweet pup will never injure another person or animal is very risky. You may also want to confirm that your policy covers you in the event the injury is away from your residence. If you have adopted the dog and have not let the insurance company know, you may be voiding the policy. Finally, it is not uncommon for insurance companies to drop insureds after even 30-40 years because of one incident – often, that is stated as ‘just put your dog to sleep.’

Defense costs in a law suit are in addition to the costs for the actual injury and/or damage. In some states you can lose everything, including your home, to pay an award to the injured party. Many dog owners believe it is only fair to take care of a person and/or animal that is injured by their dog. If any of the above concerns you or keeps you up at night, you need canine liability.

Is the coverage worth it?

It was when a visitor was mauled by an insured dog resulting in over $100,000 in medical bills. Had the coverage not been available, the cost to the dog owner would have been out of pocket.

Many people are finding landlords are willing to rent to them since the canine liability exposure can be eliminated. Most bites or injuries are situational, and even the best trained dog is still an animal. If they are put in a position where they fear for their life or yours, training will not overcome primal instinct.

Having worked with canine liability for the last 10 years, I have it for my four females, all under 10 pounds each, and I carry $300,000.

Maria Townsend

Maria Townsend

Maria TownsendMaria Townsend is an Insurance Agent helping families in NC, TX, VA, TN, and PA.

“For families who have the income to invest into pet insurance…”

You have to be mindful that insurance, period, is for unknown events. Even though most vet bills are more than the cost of insurance, pet insurance isn’t set up like health insurance for humans. In most cases, you will have to pay for vet bills upfront and the pet insurance carrier will reimburse you for the amount they promise to pay. Now, if you do decide to get pet insurance, the best time to get it is when the puppy or kitten is 6 months old. Most insurance companies do not cover pets for pre-existing conditions, but will cover the condition if it occurred during the time your pet was insured. The condition will also be covered once the policy is renewed annually just in case your dog/cat is still under care for a condition. It’s best to read the exclusions for all pet insurance policies; some only cover one surgery if the pet swallows a household object, such as a shoe or bag, and gets sick from it. Pet insurance is great for breeders, but they can’t get regular pet insurance that the average plan offers; they would have to be set up differently and it would cost more. In my experience, the best pet insurance carrier for breeders is Embrace Pet Insurance.

When buying pet insurance, some breeds cost more than others, and of course your policy will increase every year because the pet is older. Other things you want to get out of a plan are prescription coverage, wellness rewards, and flexible reimbursement. You want a flexible reimbursement plan, because you tend to not get all the care your pet needs if you have a fixed amount that the insurance company will pay for a medication or treatment.

Caleb Backe

Caleb Backe

Caleb BackeCaleb Backe is a Pet Health and Wellness Expert for Maple Holistics.

“Pet insurance is not a one-size-fits-all sort of issue….”

Different pet owners have different priorities and levels of financial freedom which can influence their decision making in terms of the health care of their pet. Some pet owners may not be able to afford the financial commitment of pet insurance, while others may be able to afford it but would rather ‘roll the dice.’

A simple rule of thumb to follow is this: If a pet owner can afford pet insurance, and knows that when the time comes they will want to foot the bill of their pet’s healthcare – no matter the issue – then pet insurance is a wise investment. If financial security is lacking, or if a pet owner is uncertain of their willingness to spend on the health of their pet, then a commitment to pet health insurance may not be the best idea.

Jeff Gitlen

Jeff Gitlen

Jeff GitlenJeff Gitlen is on the content team at LendEDU.

“To put it simply, I would recommend pet owners purchase pet insurance for their pets…”

A recent study of ours reviewed pet owners’ willingness to treat their pets for some of the most common costly conditions, and the information showed a steady decrease in willingness of owners to treat their pets as the costs rose.

A large part of this decrease in willingness is that pet owners don’t always have the funds to afford certain procedures.

Pet insurance allows these owners to feel better prepared for an unexpected illness to their pet by relieving some of the immediate financial cost.

To summarize briefly, a previous poll we conducted on this issue asked pet owners who had pet insurance if they felt it was worth it, and nearly 83% of them felt it was.

Russell Boles

Russell Boles

Russell BolesWagBrag’s co-founder, Russell Boles, has a deep history in animal rescue, welfare, and pet therapy. For the past ten years, Russ has served in various roles with two Atlanta-based animal advocacy organizations focused on rescue, training, and education.

“Here is the advice I give people about pet insurance…”

It’s not a simple answer, but if you are willing to spend thousands of dollars to save your pet’s life or on procedures that improve his/her life – then yes, absolutely pet insurance is worth having.

Besides helping with large expenses, another benefit of pet insurance is the freedom you have to select your veterinarian without restrictions. Unlike many human health plans, which require you to stay in-network for your choice of doctor, most pet insurance plans allow you select your veterinarian and then submit the claim directly to the insurance company.

Pet Insurance Review is a great source for finding and comparing insurance plans and costs. The decision about whether to invest in pet insurance can be complex, and is very tied to an individual’s circumstances.

One alternative to traditional pet insurance is a discount plan. These plans are available through companies such as PetAssure. Once you enroll, discount plans provide you with a set percentage discount off your vet visits. On the plus side, with this type of plan, pre-existing and heredity issues are covered. Also, the cost to participate in this type of plan is usually a lot less money than the typical insurance plans. However, one potential drawback is that you will be required to use a vet that is part of this plan – similar to a network. If your vet could not provide a type of required surgery or if you had an emergency, you may have no choice but to use a vet outside the network, and bear the full amount of the vet bill cost.

Steve Savage

Steve Savage

Steve SavageSteve Savage is a Senior Vice President of Business Development. He oversees all insurance industry-related new business efforts for the combined companies of LeadAmp, Clearlink, and Sykes Enterprises.

“In the last five years in particular, pet insurance has greatly increased in popularity among pet owners…”

As people have fewer children, we see the number of pets people have increase. More disposable money is being spent on our pets — from daycare and clothing, to gourmet food and day spas. Even in times of recession, people still find the dollars to pamper their pets.

Americans pay on average more than $15 billion on veterinarian care each year, with dog owners spending an average of $235 on routine vet visits, and cat owners spending an average of $196. It is also likely that a pet owner will have additional vet bills for non-routine visits each year. Depending upon the severity of the issue, expenses can easily run more than $1,000.

At the end of the day, a consumer may roll the dice and hope for very little need for pet care. But with the amount of disposable money spent on our furry friends, it is probably smart to spend a little extra on insurance to assure the health of your pet and to protect owners from catastrophic expenses.

Ali Shahid

Ali Shahid

Ali ShahidAli Shahid is a co-founder and COO at Vetted PetCare. He grew up with a slew of pets – 3 dogs, 2 cats, 2 ducks, and even a gazelle.

“A lot of people have asked me if they should get insurance for their pets. At a high-level, my answer is yes…”

Over the past few years, we have seen that costs for pet care continue to rise, and insurance is a great way to save money over the lifetime of your pet.

The reason I feel that people should invest in an insurance product is because of the bond that we share with our pets; they’re part of our family and we should never think twice about getting them care, especially if the reason comes down to the costs associated with receiving that care. While most insurance products don’t cover primary and wellness care, they can be a lifesaver when something else is needed (accidents/emergencies/tertiary care). We see that a lot of pet parents cancel their insurance policies after the first couple years because they feel that the policies gave them nothing in return for their money or because they don’t derive much value from them – I encourage you to stick on because as time goes on, the costs of tertiary care is continuing to rise. When you need your policy to kick in, your insurance company is the one who will be there to ensure that your pet gets the care they need and deserve.

A lot of people have also asked me about insurance products related to wellness and primary care. Some policies do cover wellness, but I strongly suggest that you understand what is covered and the costs associated with the care provided – it may be cheaper for you to pay out of pocket vs. paying for a wellness product from an insurance provider. If you are looking for a wellness product, you may also want to look at subscription plans from companies such as Vetted– our goal is to provide access to care at a low monthly premium where you don’t have to think twice about getting the necessary treatment your pet requires.

Tonya Wilhelm

Tonya Wilhelm

Tonya WilhelmTonya Wilhelm has been a professional in the pet community since 1998 and in the blogging world for over nine years. She has been a full-time dog training specialist for almost two decades, and she was recently named one of the top ten dog trainers in the United States.

“I’m 100% for pet insurance right out of the gate for pets…”

Emergencies or illnesses can rack up a lot of money quickly. In the case of a life-long illness, this money can be substantial. Take my dog, Dexter, for an example. Five years ago, he had an MRI and spinal tap to conclude he had Chiari-like malformation (CM) and syringomyelia (SM). That diagnosis alone cost me $4,000. Now, he has daily medications, quarterly lab work, and regular rehab sessions. Our insurance covers a huge portion of his care. Without his insurance, his treatments would have put a strain on my pocketbook, and for some, they may not be able to provide treatment because of cost. His monthly premium isn’t even close to his monthly vet care.

Lisa Schiller

Lisa Schiller

Lisa SchillerLisa Schiller is the Director Investigations and Media Relations for BBB Serving Wisconsin.

“BBB says purchasing pet insurance is a personal choice…”

But there are things you should know if you think you may purchase it.

Shop around.

Ask friends, family members, and other fellow pet owners to suggest a pet insurance provider. Ask your veterinarian if they recommend a certain pet insurance agency or plan. Check out businesses for free at bbb.org to read reviews or complaints. Make sure you are able to visit a licensed vet that is convenient for you. Insurance policies should not restrict where you are able to bring your pet for treatment.

Know what is included.

Make sure to discuss with the business exactly what is and isn’t covered by the insurance plan. If your animal’s breed is prone to genetic conditions, be sure to choose a plan that provides proper coverage for your pet. Does the policy include wellness care such as check-up exams, vaccinations, flea control, teeth cleaning, and heartworm protection? Ask if the policy covers prescription medicine, illnesses, and chronic conditions such as diabetes or cancer.

Ask if the plan uses a benefit schedule.

A benefit schedule lists the maximum amount the policy will cover for each diagnoses. Look for a policy that will reimburse you based on a percentage of the treatment cost rather than a fixed cost. In certain areas where veterinary expenses are high, the benefit schedule only covers a restricted amount of the cost and requires you to pay more money out of pocket.

Ask about pre-existing condition coverage.

Usually pet insurance policies are not responsible for covering pre-existing conditions. Ask if the plan excludes all pre-existing conditions or only “incurable” conditions. You may be able to receive partial coverage for a “curable” condition. To be on the safe side, some veterinarians recommend to get pet insurance while your pet is still young because there will be fewer pre-existing conditions to handle.

Compare costs.

Compare coverage, deductibles, co-pays, and caps between different insurance policies. Find out how much the policy will cost each month. Ask the insurance provider if they offer a deal for covering more than one pet. Ask if the cost increases each time a claim is filed or when your pet turns another year older.

Chris Middleton

Chris Middleton

Chris MiddletonChris Middleton is the President at Pets Best Insurance Services, LLC.

“There are a few things to consider when weighing whether to purchase pet insurance for your pet…”

How much did pet owners spent on veterinary care in the last year – or for whatever year data is available?

For answers to these first two questions, one of the best sources of information is the APPA’s annual industry report.

In 2016, $66.75 billion was spent on our pets in the U.S. Breakdown:

- Food: $28.23 billion

- Supplies/OTC Medicine: $14.17 billion

- Vet Care: $15.95 billion

- Live Animal Purchases: $2.1 billion

- Pet Services (grooming & boarding): $5.76 billion

Does it vary by pet, vary by age? The APPA has some data on the break down of dog vs. cat in terms of spend, but not by age that I’m aware of. You can check out the link above for this.

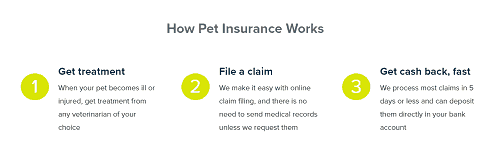

How does pet insurance work? Pet insurance is a reimbursement model, meaning the pet owner pays their bill at the veterinarian, then submits the proof of payment to us for reimbursement. On our website home page, PetsBest.com, mid-way down the page we have this:

How do you decide which policy is right for you and your pet?

- You should think about what kind of coverage is important for your pet and your budget. We offer a range of plans — a plan for accidents and illnesses, an accident only plan, and a plan for routine wellness care. Additionally, we provide plans with a variety of different annual limits and deductible and reimbursement options, including a plan with unlimited coverage, which allows pet parents to structure a plan to meet both their pets’ health care needs as well as their personal financial situation.

- You should get coverage as soon as possible, before any health issues occur with your pet, since no pet health insurer covers pre-existing conditions.

- If your pet is a senior and/or has pre-existing conditions, you may want to consider the accident only plan. Or get the accident only plan and add routine care to it.

What specific things should you look at?

- You should look at the company’s options for submitting claims. Is it going to be a cumbersome process trying to submit a claim? We recently launched our app so it’s that much quicker and easier for customers to submit claims via their phone. We also offer online claims submission in their customer account, or they can email, postal mail, or fax in their claim.

- You should look at the company’s claim processing time (turn around time or TAT as it’s called in the industry). Since pet insurance is a reimbursement model, getting your money back quickly is one of the most important features. On that note, it’s also important to look at how they will reimburse you. Some companies will only cut a check to pay your claim; so you have to factor in the time to cut the check, get it mailed to you, then deposit it. Whereas we offer direct deposit for free, so our customers can get their money back much quicker, and deposited directly into their account. But we can still cut a check if they prefer.

- You should look at whether the deductible is annual or per-incident.

- You should look at if there is exam fee coverage.

- You should look at if there is an unlimited plan option.

- You should look at if there is a routine wellness plan option. Because preventative care is important in early detection and prevention.

Emily Parker

Emily Parker

Emily ParkerEmily Parker is a cat parent to Gus and Louis, and spends too much of her time researching and writing about cats for her website, Catological.com, which helps tens of thousands of cat parents love their kitties better every month.

“Choosing whether or not to buy pet insurance depends on a number of things…”

Including your risk tolerance, your financial situation, the breed of your pet, and your pet’s lifestyle.

For most pet owners, I suggest having some money put away for unexpected vet bills, and in many cases, this comes in the form of pet insurance. However, many pet parents choose to save privately, by putting a little bit of money into a separate account every month.

The risk is that you might need more than you’ve saved if your pet needs medical attention shortly after you start saving. On the flip side, you might also never need to use that money. And unlike with insurance, you’ll get to transfer this money back into your everyday account if you don’t use it all.

I find this to be a fair middle ground for many people.

However, there’s nothing wrong with getting pet insurance, because it’s dependable, it’s a regular payment you don’t have to think about, and you can let go of the stress that comes with not knowing if you can afford veterinary bills.

The final option is not to choose pet insurance or start saving in a new account. This option is only recommended for people with a fair bit of disposable income. If a surprise multi-thousand dollar vet bill in your monthly budget won’t ruin you financially, you can opt for this route, but if not, I highly recommend either insurance or a savings account.

Whatever you choose, be sure you will be able to afford any unexpected bills, because there’s nothing worse than facing the choice between financial ruin and letting your pet suffer or even die.

Lisbet Stuer-Lauridsen

Lisbet Stuer-Lauridsen

Lisbet Stuer-LauridsenFormer Olympian, Ms Lisbet Stuer-Lauridsen, has launched a new mobile service for pet owners that will complement end of life care offered by veterinary practices. She is the Managing Director of Cloud 9 Vets.

“The answer to whether pet insurance is worth the cost depends on a few factors…”

Here is how the things stand in the UK, for example:

The average cost of owning a German shepherd over a 12-year life is just over £10,000 that assumes no serious veterinary interventions.

The average cost for insurance is £48/month i.e. £6,672 over 12 years.

The major argument for having insurance is if you dog happened to attack a third party, the legal costs alone would probably justify insurance, again this depends, it may be smart if you own a Doberman and slightly less necessary if you own a miniature poodle.

Problem is there are so many what ifs, and “it depends upon.” Pros and cons will certainly depend on the dog breed.

Chad Lovell

Chad Lovell

Chad LovellChad Lovell is the Vice President and Senior Managing Director of Strategic Partnerships, U.S. Consumer Markets, at Liberty Mutual Insurance.

“Pets are a part of our families…”

We insure ourselves and our children, so we feel it is a no brainer to extend the same protection to our pets. According to the North American Pet Health Insurance Association (NAPHIA) there are approximately 179 million pets in North America, but only 1-2 percent are insured. With all of the unexpected expenses that can occur when say, for example, your dog eats a pipe cleaner, it makes sense to have a plan in place to save yourself financial hardship down the road.

Pet insurance is absolutely worth the cost – each year one in three pets needs emergency care, and in 2016 alone $15.95 billion was spent on vet care for pets in the US. At Liberty Mutual Insurance, customers with home or auto policies can receive up to a 10 percent discount on pet insurance. The inexpensive cost of pet insurance can save customers a lot of money when accidents, injuries, or sickness to pets occur. Preventative coverage can even be added on, which can help with annual costs such as exams and vaccines.

Joel Ohman

Joel Ohman

Joel OhmanJoel Ohman is a Certified Financial Planner™ and the founder of the website InsuranceProviders.com.

“As with shopping for human health insurance…”

It is important to understand the pet insurance product that you are considering to make sure that it is a true insurance policy and not just a glorified discount plan or discount card. Health discount plans are notorious for marketing in such a way as to make you believe that they are offering a comprehensive health insurance policy and not just a discount on care and pet insurance products can be no different. It’s very important to read the fine print and understand what you are purchasing.

In the past, pet insurance was primarily a way to insure yourself against very large vet bills for things like surgeries and other expensive procedures. Recently, many pet insurance policies have become more comprehensive in nature and have added coverage on for things like regular vet check-ups – even dental care and acupuncture!

There can be a very wide range of coverage options and differences from one pet insurance policy to another so consumers will do well to carefully compare plan options and do their homework before purchasing a policy.

Danielle Salice

Danielle Salice

Danielle SaliceDanielle Salice is a pet lover, and Boxer dog aficionado — she has owned three boxers during her adult life (CarlySue, AbbySue, and Capone). She also has a penchant for German Shepherds, which was her family’s breed of choice growing up. Danielle is active in the animal welfare industry and currently volunteers at Last Chance at Life, All Breed Rescue and Adoptions. Danielle became a PetFirst Pet Insurance policyholder in 2009 and has been a pet insurance advocate ever since.

“When it came to my third Boxer, Capone, I purchased a pet insurance policy…”

And good thing I did. The first couple of years I had my pet insurance policy – he only had “minor” vet bills and pet health issues – like having a growth removed from his ear, stitches from the bite wounds he suffered from being mauled by another dog (almost $1,000), allergy testing (he’s allergic to pinto beans and milk!), an abrasion on his paw, and a couple of upset stomach issues. Sad that these are only “minor” issues to me now, because they actually racked up quite an expense, just not what I was about to deal with.

It wasn’t until Capone collapsed in January 2015 that I truly understood the value of pet insurance. In the first year he was diagnosed with a heart arrhythmia and syncope episodes, I got back $8,631.18 out of the $10,093.19 I had spent on veterinary bills. The second year I got back $10,000 from pet insurance, of the $12,689.30 I had spent on veterinary care. Without a great dog insurance policy, I wouldn’t have been able to provide Capone with the veterinary care he needed and deserved — he was a fighter and I know he lived a lot longer than anyone expected him to thanks to the vet care I was able to give him.

Chris Ashton

Chris Ashton

Chris AshtonChris Ashton is the Co-CEO of Petplan pet insurance.

“There are a few reasons to consider purchasing pet insurance…”

1. Unforeseen veterinary expenses are likely – and costly.

Taking good care of your pet will help put them on a path to a healthy life, but you can’t always see the bumps in the road. In fact, one in three pets will require unexpected veterinary care each year, and every six seconds, a pet parent is faced with a vet bill for more than $3,000. And it isn’t just older dogs and cats, either. Claims data from Petplan pet insurance shows that dogs under the age of one are actually 2.5 times more likely than their older brethren to have an unexpected visit to the vet.

2. Your pet could develop chronic health conditions.

According to claims data from Petplan pet insurance, 40% of all claims received are for chronic conditions that last beyond 12 months. Many are common health issues associated with a pet’s advancing age, such as arthritis or metabolic diseases such as diabetes or kidney failure (especially in cats). Be sure the pet insurance you select covers chronic conditions for the life of your pet as standard, so that both you and your pet can enjoy many years of comfortable companionship.

3. Veterinary costs are rising.

These days, there are more lifesaving diagnostics and treatments – like MRIs, hip replacement surgery and chemotherapy – available to our pets than ever. But with advancing veterinary medicine comes rising costs. According to the American Veterinary Medical Association, the cost of veterinary care has more than doubled over the past 10 years. Pet insurance can help keep your budget intact when you’re faced with big bills.

4. Pets are treasured members of the family.

For many of us, dogs and cats are not just pets – they’re members of the family. While every parent wants to provide their pets with the best care possible, sometimes the high costs can force you to ask for less expensive alternatives. Pet insurance can help you say yes to the treatments we recommend to get your four-legged friend back on her paws, from surgery and rehabilitative care to alternative and holistic treatments to advanced treatments like stem cell therapy and even bone marrow replacement.

5. You may be faced with difficult decisions regarding your pet’s health.

Imagine this: your pet has been hit by a car, and the vet in the emergency room says she can save her, if you act now. But the costs are considerable – max-out-your-credit-card huge. Pet insurance helps give you the peace of mind to know that you’ll never have to choose between your pocketbook and your pet. If an emergency arises, you won’t have to think twice about green-lighting lifesaving treatment, knowing your budget – and your pet – will survive.

Kathryn M. Sexton, VMD

Kathryn M. Sexton, VMD

Kathryn M. Sexton, VMDDr. Kathryn M. Sexton graduated from the University of Pennsylvania in 2009 and began practicing veterinary medicine in Chicago shortly thereafter. She joined Burr Ridge Veterinary Clinic in 2014 and appreciates that veterinary medicine continues to evolve as new treatment recommendations and medications are developed.

“Unanticipated medical issues occur daily…”

In just the last four weeks, we’ve seen four dogs with foreign bodies ranging from string to grass that required tests and surgery at an expense of more than $2,000. Since it’s unlikely most pet parents have enough spare funds to pay for life-saving surgery for their beloved pet, the veterinarians at Burr Ridge Veterinary Clinic recommend pet parents purchase insurance and urge them to select a plan with a deductible, co-pay, and policy maximum that is right for their four-legged family member’s breed, lifestyle and personality. Dogs and cats of any age will chew and swallow just about anything that doesn’t taste bad and, when that happens, immediate diagnostics and treatment can be the difference between saving a life or having to say goodbye to a furry best friend.

Peter Marcia

Peter Marcia

Peter MarciaMr. Marcia assumed an active role in the management of YouDecide in mid-2006 after two years as an investment partner. Prior to his involvement with YouDecide he was Vice President and National Director of Employee Benefits for Hilb, Rogal and Hobbs, the world’s 10th ranking broker, where he led the company’s strategic business unit. Previously, he led the employee benefits practices of Hobbs Group, LLC, in Atlanta and O’Neill, Finnegan & Jordan of Boston.

“Pet owners know that a trip to vet can become very expensive…”

Pet insurance can help provide pet owners with peace of mind knowing that some of the costs of an unexpected illness or injury will be taken care of. Depending on the plan, some pet insurance programs will provide coverage for more routine care, such as teeth cleaning or flea prevention. Premiums for pet insurance are often based on the type, breed and age of the pet as well as where you live, so it is always wise to get an estimate and then determine for yourself whether the cost is worth it.

Wendy Hauser, DVM

Wendy Hauser, DVM

Wendy Hauser, DVMWendy Hauser is the AVP of Veterinary Relations for ASPCA Pet Health Insurance.

“Pet health insurance helps pet parents to…”

Provide the care they feel is appropriate for their animals, with less emotional stress of financial limitations. We encourage pet parents to get their pet insured while they are young and healthy, before anything happens.

Nick Braun

Nick Braun

Nick BraunNick is the founder of PetInsuranceQuotes.com. He is a serial entrepreneur with over 15 years of experience in finance and insurance. Nick has been involved in the pet insurance industry for over a decade and has held various roles.

“Pet insurance is a great investment for pet owners who would do anything for their pets…”

In other words, if a dog or cat owner is willing to spend $5,000, $10,000 or more on veterinary treatment then it’s a no-brainer.

The average plan is only $41/month (depending on your pet’s age and breed) or about $492/year. Serious health issues like cancer, heart disease and torn ligaments can cost $5,000 or more. With just one major health issue during a pet’s lifetime could be worth 10 years of pet insurance payments.

The best time to purchase a plan is when you first get your pet to ensure there are no pre-existing conditions issues. This way there won’t be any coverage exclusions as long as you own your pet.

Clint Lawrence

Clint Lawrence

Clint LawrenceClint Lawrence is the Vice President of Sales for PetFirst.

“Like people, dogs and cats are going to get sick or injured…”

Our pets are living longer and veterinarians are able to treat for more today than they could in the past. As a result of better technology and more treatments veterinary costs have increased. Pet insurance is not for the day-to-day, or routine, costs of owning and caring for a dog or cat. Those are the costs that you can budget or predict. Pet insurance is for the unplanned accident or illness that can cost thousands of dollars. It’s important to have a plan in place when a large vet bill happens. And hopefully, as with other forms of insurance, you never have to use it.

JaneA Kelley

JaneA Kelley

JaneA KelleyJaneA Kelley is the author of the award-winning cat advice blog, Paws and Effect. She is a contributing author for Catster Magazine and a member of the Cat Writers’ Association. Her story “Belladonna: Sweet Sugar Kitty” appears in Rescued Volume 2, an anthology of 12 rescue cats’ stories told from the cats’ point of view.

“I absolutely believe pet insurance is worth the cost because…”

I know what veterinary care costs, and the cost of pet insurance is chump change compared to the cost of treatment for any serious injury or illness. I found out about this the hard way. I didn’t think about pet insurance at all before my cat, Dahlia, got very sick with lymphoma. I spent several thousand dollars on her care, and that was five years ago in a small city. The same care in a large city today could go well into the five-digit numbers.

Pet insurance saves lives. I worked at a pet insurance company for two years and I saw this happen every day. I can’t even tell you how many policyholders told me, “I’m so glad I have the insurance, because if I hadn’t, I would have had to put my pet down.”

Some people figure they’ll start a savings account to cover veterinary care costs. While that’s a great option if you can do it, a lot of us can’t. If you start a savings account, you may have another emergency that requires the money you’ve saved for your pet’s care. And what happens if you start saving, say, $50 a month, and a few months into your savings you get hit with a $5,000 vet bill?

Simply put, pet insurance provides peace of mind. I never want to be in a position where I have to euthanize one of my beloved cats simply because I couldn’t afford the care that would provide a good quality of life. After the painful lessons I learned with Dahlia, I carry pet insurance for all of my cats, and I’ll never be without it again.

Dr. Sarah Nold, DVM

Dr. Sarah Nold, DVM

Dr. Sarah Nold, DVMSarah Nold, DVM completed her BS in Biology and Science at Portland State University before attending Oregon State University College of Veterinary Medicine. She graduated in 2010 and immediately moved up to Washington where she worked in small animal clinical medicine before joining the Trupanion team. She has two cats, George and Juniper.

“We all love our pets…”

In fact, our pets are considered part of the family and we would do anything to give them a long, happy, healthy life. Just like with health insurance for other members of the family, medical insurance for a pet helps owners give their pet the best care, without worrying about the cost.

Depending on the plan, medical insurance for your pet can cover almost anything – from allergies to hereditary and congenital conditions. Also, coverage may include holistic and alternative therapies.

Today with advances in veterinary medicine, that provides pets the same access to cutting-edge diagnostics and treatments available in human medicine, unplanned illnesses can easily cost thousands of dollars. For example, a knee ligament rupture on a dog can cost almost $3,000 to repair.

We all hope that our pet will be lucky and avoid any major illnesses or injuries. But in reality there’s no way to predict whether your pet will be lucky or unlucky. If something happens to your pet, you should be able to focus on helping them heal without thinking about your wallet. Medical insurance for your cat or dog provides peace of mind when you need it most.

Bottom line: Veterinarian care can be costly and medical insurance for pets helps remove that burden so owners can make the best decision for their pet regardless of cost.

Rob Jackson

Rob Jackson

Rob JacksonRob is the co-founder and chief pet protector of Healthy Paws Pet Insurance. Rob and Co-Founder Steve Siadek met through a local, no-kill animal shelter. As pet parents they envisioned a business that respected pets as family, as well as the development of a foundation to help homeless dogs and cats. Over his 30-year career, Rob has been an entrepreneur, insurance executive, and non-profit devotee.

“Keeping pet care costs down over the long-term means committing to preventative care, seeing your vet annually to nip conditions in the bud, and enrolling in pet insurance as early as possible to avoid pre-existing conditions…”

Preventative Care: Just like humans, everything from dental check-ups to vaccines help your pet live a longer, healthier life. With cats and dogs, preventative care safeguards their basic health, protecting them from big diseases like heartworm or rabies, helping you avoid expensive complications later. While you can’t prevent every accident or illness, taking these precautionary steps can save a lot of stress for both you and your pet further down the road.

Annual Vet Visits: Preventative care goes hand-in-paw with your pet’s annual vet visits. A quick physical and a few tests can rule out any illnesses in the early stages, possibly saving your pet’s life. Again, just like humans, discovering illnesses in their earliest stages means a better chance for recovery and survival.

Enrolling in Pet Insurance: As soon as you adopt your pup or kitten, enroll them in pet insurance. Getting coverage before any illnesses or chronic conditions arise will help you avoid pre-existing conditions that can be excluded from coverage down the line. Healthy Paws Pet Insurance coverage is provided with no limits on claims; so, if your pet needs treatment for an accident or illness, and it’s not a pre-existing condition, it’s covered. This includes not just accidents and one-off illnesses but also hereditary, congenital, and chronic conditions, diagnostics, x-rays, and prescriptions. Pet insurance premiums vary depending on the breed of your dog or cat. Mixed breeds tend to be healthier and have lower premiums, which is a great reason to consider rescuing a mutt!

Unexpected Pet Health Emergencies: A limping injury may need diagnostic tools like x-rays and MRIs that can run up to $5,000. We regularly see small claims – an allergy diagnosis and treatment may be $250 – as well as catastrophic claims – spinal diseases that can run over $40,000. With veterinary science evolving to treat our pets better and faster, the price tag is higher as well. Pet insurance protects your pets by giving you the financial freedom to seek out the best care possible.

Pet Insurance Reviews

See each of our in-depth reviews of all pet insurance companies below:

- Embrace Pet Insurance Review

- Healthy Paws Pet Insurance Review

- Pet Assure Pet Insurance Review

- PetFirst Pet Insurance Review

- Pets Best Pet Insurance Review

- Trupanion Pet Insurance Review

Featured Image Credit: savitskaya iryna, Shutterstock